Corporate Governance

- 02 Feb 2024

- 27 min read

For Prelims: Good Governance, Corporate Governance, Companies Act, 2013, SEBI Listing Obligations and Disclosure Requirements (LODR), Whistleblower Protection, Satyam Scam Case, Standing Committee on Finance, Companies Law Committee, Infosys, Tata Group, Insider Trading, Minority Shareholders, Board of Directors, Board Committees, Non-Financial Disclosure, Ministry of Corporate Affairs (MCA), IL&FS Crisis, National Company Law Appellate Tribunal (NCLAT), Corporate Social Responsibilty, Environmental, Social, and Governance (ESG).

For Mains: Importance of Corporate Governance in promoting ethical practices and transparency and accountability in corporate sector.

What is the Context?

Corporate governance and ethics are two interrelated concepts that play a crucial role in shaping the behavior and decision-making processes within organizations. The relationship between corporate governance and the importance of ethics is fundamental to maintaining transparency, accountability, and sustainable business practices.

Ethics is closely linked to transparency and accountability, two pillars of good corporate governance. An ethically governed organization is more likely to provide accurate and transparent information to stakeholders.

What is Corporate Governance?

- About:

- Corporate governance is the set of rules and processes that guide how a company is managed and overseen. It’s vital for ensuring that businesses operate ethically and in the best interests of those involved. A primary goal of corporate governance is to prevent corporate greed and promote responsible and transparent business practices.

- By establishing and enforcing high ethical standards and holding individuals accountable for their actions, corporate governance serves as a safeguard against misconduct, protecting the interests of shareholders, customers, and the wider community.

- Principles of Corporate Governance:

- Fairness: The board of directors must treat shareholders, employees, vendors, and communities fairly and with equal consideration.

- Transparency: The board should provide timely, accurate, and clear information about such things as financial performance, conflicts of interest, and risks to shareholders and other stakeholders.

- Risk Management: The board and management must determine risks of all kinds and how best to control them. They must act on those recommendations to manage them. They must inform all relevant parties about the existence and status of risks.

- Responsibility: The board is responsible for the oversight of corporate matters and management activities.

- It must be aware of and support the successful, ongoing performance of the company. Part of its responsibility is to recruit and hire a Chief Executive Officer (CEO). It must act in the best interests of a company and its investors.

- Accountability: The board must explain the purpose of a company’s activities and the results of its conduct. It and company leadership are accountable for the assessment of a company’s capacity, potential, and performance. It must communicate issues of importance to shareholders.

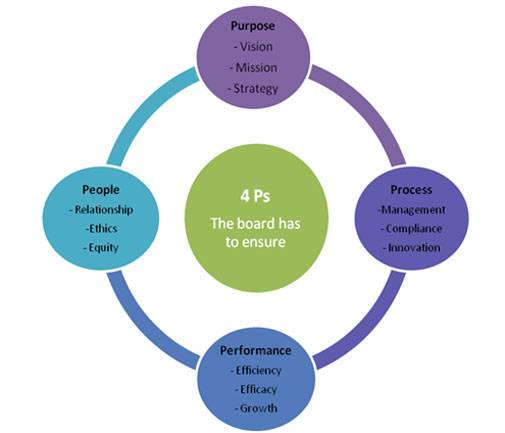

- Four Ps of Corporate Governance:

- People: This ‘P’ emphasizes the importance of the individuals involved in corporate governance, including the board of directors, executives, and employees. The composition of the board, their skills, independence, and diversity are crucial factors.

- Purpose: Purpose refers to the overarching mission and goals of the company. Corporate governance ensures that the company’s purpose aligns with ethical standards and is focused on creating long-term value for shareholders and stakeholders.

- Processes: This ‘P’ involves the systems and procedures established to oversee and manage the company. Governance processes include how decisions are made, how risk is assessed and managed, and how accountability is maintained.

- Practices: Performance in corporate governance relates to the company’s overall success in achieving its goals while adhering to ethical standards. The governance framework monitors and evaluates the performance of the company against established benchmarks.

What are the Key Components of Corporate Governance?

- Board of Directors:

- Composition and Independence:

- The number of directors can vary depending on the size of the company. The board of directors must have a minimum of three directors if it is a public company, two directors if it is a private company, and one director in a one-person company. The maximum number of members a company can assign as directors is fifteen.

- At least one director, who has lived in India for a minimum of 182 calendar days of the previous year, shall be appointed by every company’s board. It is a mandatory rule.

- At least, one woman director must be appointed by the company. All listed companies must have at least one-third proportion of their board of directors as independent directors.

- Board Committees:

- Board committees are sub-groups of the board of directors that are formed to focus on specific areas of responsibility. Not every board of directors has committees, but they are common in larger organisations.

- Some of the most common board committees include audit committees, compensation committees, and nominating committees.

- Board committees are sub-groups of the board of directors that are formed to focus on specific areas of responsibility. Not every board of directors has committees, but they are common in larger organisations.

- Composition and Independence:

- Shareholders and Stakeholders:

- Rights and Responsibilities:

- Shareholders have the right to vote on important company decisions, such as electing the board of directors, approving mergers and acquisitions, and making changes to the company’s articles of incorporation.

- They also have the right to receive dividends and to inspect the company’s books and records.

- Minority Shareholder Protection:

- Minority shareholders are shareholders who own less than 50% of a company’s shares and do not have full control over the corporation.

- However, they still have the right to vote and can hold directors and officers accountable for their actions, which ultimately leads to greater efficiency and increases financial returns.

- Rights and Responsibilities:

- Disclosure and Transparency:

- Financial Reporting:

- Financial reporting is the process of disclosing financial information to stakeholders. It includes the preparation of financial statements, such as balance sheets, income statements, and cash flow statements.

- Financial reporting is governed by various accounting standards, such as Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

- Financial reporting is the process of disclosing financial information to stakeholders. It includes the preparation of financial statements, such as balance sheets, income statements, and cash flow statements.

- Non-Financial Disclosure:

- Non-financial disclosure refers to the disclosure of information that is not directly related to a company’s financial performance. This can include information about a company’s Environmental, Social, and Governance (ESG) practices.

- Financial Reporting:

What are Environmental, Social and Governance (ESG) Goals?

- ESG goals are a set of standards for a company’s operations that force companies to follow better governance, ethical practices, environment-friendly measures and social responsibility.

- Environmental criteria consider how a company performs as a steward of nature.

- Social criteria examine how it manages relationships with employees, suppliers, customers, and the communities where it operates.

- Governance deals with a company’s leadership, executive pay, audits, internal controls, and shareholder rights.

- It focuses on non-financial factors as a metric for guiding investment decisions wherein increased financial returns is no longer the sole objective of investors.

- Ever since the introduction of the United Nations Principles for Responsible Investing (UNPRI) in 2006, the ESG framework has been recognised as an inextricable link of modern-day businesses.

- ESG Framework relates to intangible aspects of corporate governance unlike Corporate Social Responsibility (CSR) which fufils the tangible aspects through implementation of projects.

- In developing economies like India, CSR is seen as part of corporate philanthropy in which corporations augment the social development to support the initiatives of the government and it also synchronises the concept of good governance with corporate governance.

What is the Regulatory Framework for Corporate Governance in India?

- Evolution of Regulatory Framework:

- Regulatory Authorities for Corporate Governance:

- The Ministry of Corporate Affairs (MCA) and the Securities and Exchange Board of India (SEBI) play pivotal roles in overseeing corporate governance initiatives in India.

- Their responsibilities encompass establishing and enforcing regulations to ensure ethical business practices and safeguard the interests of stakeholders.

- Corporate Governance Regulation:

- In the 1990s, SEBI took charge of regulating corporate governance through key laws such as the Security Contracts (Regulation) Act, 1956; Securities and Exchange Board of India Act, 1992; and the Depositories Act of 1996, marking a crucial period of regulatory development.

- Introduction of Formal Regulatory Framework:

- In a landmark move in 2000, SEBI instituted the first formal regulatory framework for corporate governance in response to recommendations from the Kumar Mangalam Birla Committee, 1999.

- This initiative aimed to enhance corporate governance standards in India and laid down guidelines for transparent and accountable business practices.

- Subsequent Governance Initiatives:

- Building on these developments, a significant corporate governance initiative unfolded in 2002 when the Naresh Chandra Committee on Corporate Audit and Governance extended its recommendations to address various governance issues.

- Notable examples include setting up the Confederation of Indian Industry (CII), National Foundation for Corporate Governance (NFCG), and the Institute of Chartered Accountants of India (ICAI), all working collectively to foster responsible and transparent corporate practices in the country.

- Building on these developments, a significant corporate governance initiative unfolded in 2002 when the Naresh Chandra Committee on Corporate Audit and Governance extended its recommendations to address various governance issues.

- Regulatory Authorities for Corporate Governance:

- Companies Act, 2013:

- Provisions Related to Corporate Governance:

- These provisions include greater accountability on companies through the appointment of Key Managerial Personnel (KMPs), the role of audit committees, independent audits, stricter regulation of related party transactions, and restrictions on layers of companies.

- Enhanced disclosures are mandated, including through the board’s report, financial statements, and filings with the Registrar of Companies, to ensure that all relevant information is available to investors and regulatory agencies.

- Amendments and Updates:

- Some of the key amendments include the introduction of the National Company Law Tribunal (NCLT) and the National Company Law Appellate Tribunal (NCLAT) to replace the Company Law Board, the introduction of the Insolvency and Bankruptcy Code, 2016.

- The amendment of the definition of “related party” to include entities holding equity shares of 10% or more in the listed entity either directly or on a beneficial interest basis.

- The Act has also been amended to provide for the appointment of an independent director in case of a company with a paid-up share capital of ten crore rupees or more, and the requirement of a special resolution for the appointment of an auditor.

- Provisions Related to Corporate Governance:

- National Financial Reporting Authority (NFRA):

- NFRA is an Indian regulatory body that was established in 2018, under section 132 of the Companies Act, 2013. The duties of the NFRA include recommending accounting and auditing policies and standards to be adopted by companies for approval by the Central Government etc.

What are the Ethical Challenges Associated with Corporate Governance?

- Selection Procedure and Term of Board: The selection of board members and their term is highly misused in Indian corporate governance.The term of the board members should be long enough to ensure stability, but not so long that they become complacent.

- For example, the Tata-Mistry fallout in 2016 was due to the disagreement between Cyrus Mistry and the board of Tata Sons over the appointment of independent directors.

- Performance Evaluation of Directors: The performance evaluation of directors is a challenging aspect of corporate governance. It helps to identify areas of improvement and ensure that the board is functioning effectively. However, the evaluation process should be transparent and objective.

- For example, in 2018, SEBI directed listed companies to disclose the criteria for evaluating the performance of independent directors.

- Missing Independence of Directors: In many cases, the independence of directors is compromised due to their close association with the promoters or management.

- For example, in 2018, the ICICI Bank controversy arose when it was alleged that the bank’s CEO had approved a loan to Videocon Industries in exchange for a quid pro quo deal for her husband.

- Removal of Independent Directors: The removal of independent directors is a serious issue in corporate governance. It is important to ensure that independent directors are not removed for raising concerns or dissenting opinions.

- For example, in 2018, the board of Fortis Healthcare removed its independent director after he raised concerns over the company’s acquisition by IHH Healthcare.

- Liability Toward Stakeholders: In many cases, companies prioritize the interests of their promoters or management over the interests of their stakeholders.

- For example, in 2019, the Infrastructure Leasing & Financial Services (IL&FS) crisis occurred due to the company’s mismanagement and failure to meet its financial obligations to its stakeholders.

- Founder/Promoter’s Extensive Role: The role of the founder or promoter in the company’s governance can be a double-edged sword. While their vision and leadership can be beneficial, their extensive role can lead to conflicts of interest and lack of transparency.

- For example, in 2019, SEBI directed companies to disclose the reasons for the appointment of the founder or promoter as the chairman of the board.

- Transparency and Data Protection: Lack of transparency and inadequate data protection are the harmful corporate practices. They should ensure the protection of sensitive data and information.

- For example, in 2018, the Reserve Bank of India (RBI) directed banks to ensure the protection of their customers’ data and information.

- Business Structure and internal conflicts: The business structure and internal conflicts are often visible in corporate sector. Companies should have a clear and well-defined business structure to avoid conflicts of interest. They should also have mechanisms in place to resolve internal conflicts.

- For example, in 2019, the board of IndiGo Airlines had a public spat over the appointment of its CEO, which led to concerns over the company’s corporate governance.

- Conflict of Interest: The challenge of managers potentially enriching themselves at the cost of shareholders is a significant issue in corporate governance.

- For example, in 2018, SEBI directed companies to disclose the details of related party transactions.

- Weak Board: Lack of diversity of experience and background represents a major area of weakness for these boards. Companies should ensure that their board members have diverse backgrounds and experiences to ensure effective decision-making.

- For example, in 2018, SEBI directed companies to have at least one woman director on their board.

- Insider Trading:

- Insider Trading occurs when corporate insiders, such as officers, directors etc use confidential information to make personal profits. The problem arises because SEBI lacks a robust investigative mechanism and a vigilant approach, enabling culprits to escape.

What are the Reforms Needed in Corporate Governance?

- Strengthening Board Independence:

- Ensure a balanced board composition with a substantial number of independent directors who can provide unbiased perspectives.

- Conduct periodic assessments of the board’s performance and individual director effectiveness.

- Infosys is often cited as a benchmark for corporate governance in India. The company has a strong board structure, with a majority of independent directors.

- Enhancing Transparency and Disclosure:

- Implement rigorous financial reporting practices to provide stakeholders with accurate and timely information.

- Disclose non-financial information, such as ESG factors, to give a holistic view of the company’s performance.

- Tata Sons, the holding company of the Tata Group, has a history of transparency and adherence to governance norms. The removal of Cyrus Mistry as the Chairman in 2016 and subsequent legal battles highlighted the group’s commitment to governance principles.

- Empowering Shareholders:

- Encourage the use of proxy advisory services to facilitate informed shareholder decision-making, especially during critical votes.

- Promote shareholder activism to hold the board and management accountable for their actions.

- Effective Risk Management:

- Establish a dedicated committee to identify, assess, and manage risks, ensuring that potential threats to the business are proactively addressed.

- Conduct regular risk assessments to stay ahead of emerging risks and vulnerabilities.

- Ethical Conduct and Compliance:

- Develop and enforce a comprehensive code of ethics that outlines expected behavior and ethical standards for all employees and stakeholders.

- Implement a robust whistleblower mechanism to encourage the reporting of unethical practices without fear of retaliation.

- Executive Compensation Policies:

- Align executive compensation with the company’s performance to ensure that leaders are motivated to drive sustainable growth.

- Clearly disclose executive compensation structures to shareholders, promoting accountability.

- Corporate Social Responsibility (CSR):

- Integrate socially responsible practices into business operations and disclose CSR activities to showcase the company’s commitment to broader societal well-being.

- Board Training and Development:

- Provide ongoing training for board members to keep them updated on industry trends, regulatory changes, and governance best practices.

- Develop a robust succession plan for key leadership positions to ensure continuity and stability.

- Regulatory Compliance:

- Conduct regular audits to ensure compliance with all relevant laws and regulations.

- Follow established corporate governance codes and guidelines set by regulatory authorities.

- Engagement with Stakeholders:

- Foster open communication with stakeholders, including shareholders, employees, and customers, to build trust and transparency.

- Actively seek and consider feedback from stakeholders to address their concerns and expectations.

- Mahindra & Mahindra is known for its commitment to ethical business conduct and sustainability. The company’s governance practices focus on stakeholder engagement and risk management.

What are Committee Reports and Supreme Court Judgments on Corporate Governance?

- Kotak Panel Report: The panel constituted by SEBI under the chairmanship of Uday Kotak has suggested a host of changes for improving corporate governance standards of firms in 2017:

- Chairman of the board cannot be the Managing Director/ CEO of the company.

- Boards should have minimum of six directors. Of these 50% should be independent directors including at least one woman independent director.

- Mandate minimum qualification for independent directors and disclose their relevant skills.

- Create a formal channel for sharing of information between the company and its promoters.

- Public sector companies should be governed by listing regulations, not by the nodal ministries.

- Auditors should be penalized if lapses are found.

- SEBI should have powers to grant immunity to whistleblowers. Companies should disclose medium-to-long term business strategy in annual reports.

- TK Viswanathan Committee: The recommendations of TK Viswanathan committee on fair market conduct which submitted its report in 2018 are:

- Among a number of recommendations on insider trading, is the creation of two separate codes of conduct.

- Minimum standards on dealing with insider information by listed companies.

- Standards for market intermediaries and others who are handling price-sensitive information.

- Companies should maintain details of immediate relatives of designated persons who might deal with sensitive information and of people with whom the designated person might share a material financial relationship or who share the same address for a year.

- Such information may be maintained by the company in a searchable electronic format. It may also be shared with the SEBI when sought on a case-to-case basis.

- The committee has recommended direct power for SEBI to tap telephones and other electronic communication devices. This is to check insider trading and other frauds.

- Currently, SEBI has the power to only ask for call records including numbers and durations.

- Among a number of recommendations on insider trading, is the creation of two separate codes of conduct.

- Kumar Mangalam Birla Committee Report, 2000:

- Some of the key recommendations of the report include:

- The separation of the roles of Chairman and CEO.

- The appointment of independent directors to the board of directors.

- The establishment of an audit committee to oversee financial reporting.

- The requirement for companies to disclose their financial and non-financial performance.

- The establishment of a code of conduct for directors and senior management.

- Some of the key recommendations of the report include:

- Supreme Court Judgements:

- Satyam Computer Services Ltd. Fraud (2009):

- Satyam’s founder and chairman, Ramalinga Raju, admitted to inflating the company’s financial statements and engaging in accounting fraud.

- The Supreme Court’s intervention led to a reconstitution of the board and management of Satyam and highlighted the need for robust corporate governance mechanisms.

- SEBI v. Sahara (2012):

- The Sahara case involved a long-standing dispute between SEBI and Sahara Group regarding the issuance of optionally fully convertible debentures (OFCDs).

- The Supreme Court emphasized the importance of protecting the interests of investors and ensuring compliance with securities laws. This judgment had implications for corporate fundraising practices.

- Satyam Computer Services Ltd. Fraud (2009):

Conclusion

Addressing the multifaceted aspects of corporate governance in India requires a holistic approach involving legal reforms, regulatory enhancements, and a cultural shift towards ethical business practices. Continuous monitoring and adaptation to evolving global standards are imperative for sustaining investor trust and fostering economic growth.

UPSC Civil Services Examination Previous Year Question (PYQ)

Q1. In the light of the Satyam Scandal (2009), discuss the changes brought in corporate governance to ensure transparency and accountability. (2015)

Q2. What do you understand by the terms ‘governance’, ‘good governance’ and ‘ethical governance’? (2016)